Embarking on the journey of buying a house for the first time can feel both intimidating and exciting.

Acquiring adequate knowledge about the process is paramount, particularly for first-time home buyers.

With so many elements to consider, I will share fundamental steps that can guide you smoothly through this transition.

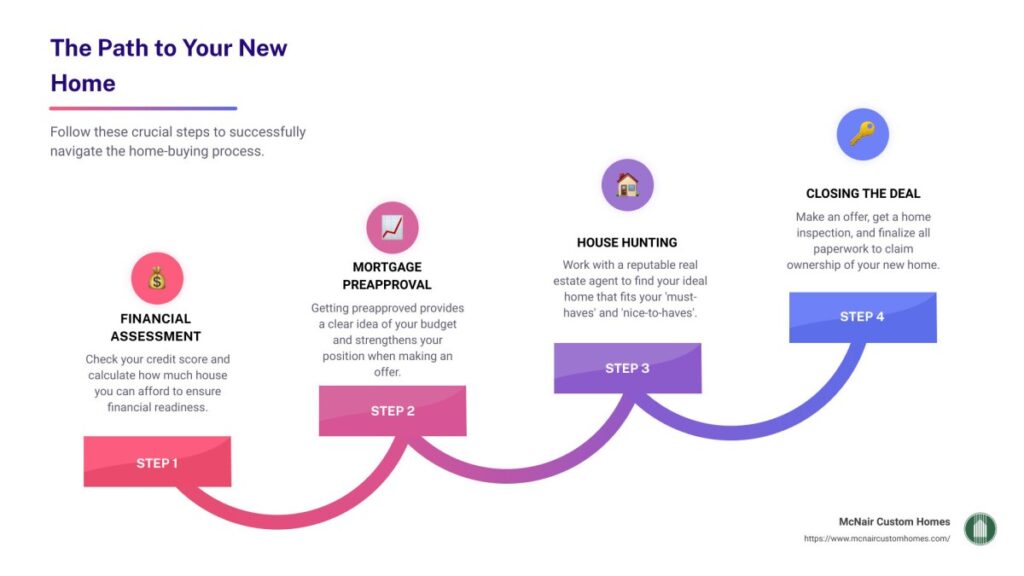

In order to better understand this process, here’s a glance at some crucial aspects:

- Determine Your Readiness: Assess your financial capability and readiness to take on a mortgage.

- Identify Suitable Properties: Look for homes that match your preferences and budget range.

- Mortgage Pre-Approval: Secure pre-approval from a financial institution to strengthen your position as a buyer.

- Select a Real Estate Agent: Partnering with an experienced agent can greatly ease the process for rookie buyers.

- Submitting a Purchase Offer: Once you find your desired property, offer a bid that suits your budget and market value predictions.

- Securing Your Mortgage: Finalizing your mortgage secures your dream home after the purchase offer is accepted.

This brief guide should help steer first time buyers in the right direction.

Contents

A Quick Tip For First-Time Home Buyers

The banking sector and real estate market are rapidly evolving; hence, staying informed is crucial.

Eager buyers may find this article on how fast house sales could happen in 2024 enlightening.

Educate yourself about current trends and other relevant factors before acting.

Remember, patience and thorough planning will lead you to your dream home.

Determine Your Readiness

Knowing if you’re ready for homeownership goes beyond being prepared financially, it’s also about emotional readiness.

Are you prepared to settle in a single place and adapt to a new lifestyle and neighborhood?

This commitment often involves handling long-term financial obligations.

| Emotional Factors |

|---|

| Commitment to a new lifestyle |

| Setting roots in one place |

| Long-term financial commitments |

| Familiarizing yourself with the process |

| Your emotional readiness plays a key role in your home-buying decision. |

It’s essential to decipher these emotions before taking the leap into property ownership.

Let’s also talk about financial preparedness. Striving for a credit score of 700 or higher can offer better loan options.

| Financial Preparedness |

|---|

| Aim for high credit score (700+) |

| Savings for down payment, costs, and ongoing expenses |

| Maintain Debt-to-Income ratio below 43% |

| Budget for insurance, taxes and maintenance |

| A good grasp on your financial standing allows smoother property purchase transactions. |

To get favorable deals, it’s good practice to familiarize yourself with different down payment options and interest rates.

Get acquainted with government loans such as FHA, VA, and USDA loans. Private Mortgage Insurance (PMI) is equally important, so understand when it’s mandatory and how it affects your mortgage.

Moreover, learn to differentiate between pre-approval and pre-qualification during the mortgage process. A good understanding of the home inspection protocol comes in handy during negotiations.

Knowing the appraisal process and adjusting your estimations for closing costs can keep unexpected expenses at bay.

| Home Financing Knowledge |

|---|

| Different down payment options |

| Interest rates impact on mortgage |

| Benefits of FHA, VA & USDA loans |

| Understanding PMI |

| Home financing knowledge significantly boosts your homeownership readiness. |

To read about more insights into first-time home buying, you can visit this link.

Establish Your Budget

Understanding your financial standing is vital as a first-time homebuyer. This knowledge allows you to devise a budget, crucial for homeownership expenses.

Your credit score determines your eligibility for a mortgage and its interest rate. Aim for a credit score of no less than 620.

A higher credit score benefits you with more attractive loan terms and lower interest rates. It places you in a better position for negotiation.

Calculate your earnings, fixed expenditure, and discretionary spending to ascertain what mortgage payment is affordable for you. Ideally, it should be under 28% of your pretax income.

| Credit Score | Significant Factors | Suggestions |

|---|---|---|

| Above 620 | Eligibility for conventional mortgages | Maintain or increase the score |

| Less than 620 | Possible higher interest rates | Work towards improving it |

| High Score | Favorable loan terms | Maximize benefits during negotiations |

| Affordability Index | Mortgage account for less than 28% of pre-tax income | Plan budget accordingly |

| Budgeting | Incomes vs expenses calculation | Ascertain affordability of mortgage payment |

| Table: Importance of credit score in home buying | ||

Remember to account for property taxes, insurance premiums, maintenance costs and utilities when budgeting for your home.

Try to aim for a down payment of 20% to avoid Private Mortgage Insurance (PMI). Also, take into consideration the closing costs which usually falls between 2% and 5% of the purchase price.

The Federal Housing Administration (FHA) offers assistance programs that you may want to consider. These programs can considerably lighten your financial load.

Including your stable income and variables like bonuses or seasonal income towards the budget is crucial. Similarly, consider consistent monthly expenses like rent, utilities, along with loan payments.

Factor in less predictable expenses like entertainment or dining out. This helps in planning a comprehensive and realistic budget.

It’s equally important to allocate funds for emergency savings, retirement, amongst other personal goals. This aids in maintaining financial stability in the long run.

You need to plan for annual property tax hikes and various insurance premiums, such as homeowners and flood insurance. Remember, staying prepared helps avoid unpleasant surprises.

Identify Suitable Properties

Identifying appropriate properties as a first-time homebuyer can appear daunting. An initial step toward formation of a fruitful strategy is ensuring readiness.

- Assess Personal Stability: Are you in stable employment? Can you envision residing in the same town for the next decade?

- Consider Property Requirements: Determine your immediate needs such as location, number of rooms, or yard space.

- Determine Affordability: Be sure to request your credit report and correct any discrepancies as soon as possible.

- Gather Documentation: This could include proof of employment, bank statements, past tax returns, and current landlord references.

Post readiness evaluation, the next step involves creating a wish list for your ideal home.

Analyze what’s essential to you in different neighborhoods, dwellings,

The next step would be figuring out what you can afford.

Request your credit reports, assessing the excellence of the down payment and estimating potential maintenance costs come to play.

Compiling necessary documents follows this step. Gather pay stubs, tax returns and proof of address to start with.

In terms of financial assistance, do shop around for the best mortgages on offer. Start by getting pre-qualified and follow it up with obtaining pre-approval letters.

The final stage involves assembling an efficient team to support you through the process. This could include a trusted real estate agent or a friend who is knowledgeable about property buying for advice and second opinions.

This detailed list will aid novices in making informed decisions while hunting for auspicious properties that suit their needs and provide a convenient living environment.

Explore Financing Options

Embarking on your journey to home ownership may be daunting, particularly for the crucial aspect of financing. You might be unsure if you should choose an adjustable or fixed rate mortgage, or if a government-backed loan would be more beneficial.

Contrary to common perception, a wealth of financing options are accessible to first-time house buyers, not just your conventional loans.

- Adjustable Rate Mortgages (ARMs): These have varying interest rates. Examples include 1-Year ARM where interest changes annually, and 3/1, 5/1, 5/5 ARMs that come with a set fixed rate for three, five or ten years before adjustments occur.

- Fixed Rate Mortgages: They provide steady interest rates with predictable monthly payments. A Conventional Fixed Rate Mortgage and 15-Year or 30-Year Fixed Rate Mortgages are among the popular choices.

- Government-Backed Programs: These loans offer great benefits like smaller down payment requirements and lenient credit qualifications. The FHA Loan, VA Loan and USDA Loan are examples.

- Additional Financing Options: These encompass unique arrangements like the Balloon Mortgage with lower initial payments leading to a larger sum due later.

To make an informed decision, it’s essential to understand each option’s pros and cons. For instance, ARMs can offer lower initial interest rates but may pose risks when market rates rise. On the other hand, fixed-rate mortgages give you predictable payments at the expense of typically higher initial rates.

Government-backed loans are attractive because of their relaxed eligibility criteria and possibly even no down payment requirement like in the case of VA loans. Yet, they often come with limits on loan amounts or property types.

There’s a right mortgage for everyone. Understand your financial circumstances, evaluate the options, and make a prudent choice. More helpful advice and intricate details on these may be found at this informative guide prepared for first-time home buyers.

Mortgage Pre-Approval

Obtaining pre-approval entails submitting a mortgage application and providing your Social Security number, so the lender can perform a hard credit check. This process can be thrilling, nerve-racking, and perplexing.

Some online lenders may grant pre-approval within hours, whereas some might require several days. The duration is dependent on the lender and the intricacy of your financial situation.

The mortgage application you fill out will request your identification data, including your Social Security number, so the lender can examine your credit.

The stipulated mortgage credit checks comprise a hard inquiry on your credit reports, which could affect your credit score. However, if you’re examining numerous lenders within a short timeframe (45 days according to newer FICO scoring models), these combined credit checks are accounted as a single inquiry.

Additionally, when applying with another borrower whose income you need for qualifying for the loan, both must provide their financial and employment data. The uniform mortgage application comprises eight primary sections:

The particulars of the loan for which you’re applying; the loan amount; terms like repayment time (amortization); and the rate of interest come under ‘Type of Mortgage and Terms of Loan’.

‘Property Information and Purpose of the Loan’ encompasses details like address; legal description of the property; year built; loan purpose whether its purchase, refinance, or new construction; and intended type of residency: primary, secondary or investment.

‘Borrower Information’ seeks personal details including full name, date of birth, Social Security number among others while ‘Monthly Income and Combined Housing Expense Information’ gives an account of your complete monthly income details and combined housing expenses.

A noteworthy point is that although a mortgage pre-approval does not necessarily promise a loan, pre-approval letters are conditional on the authenticity and consistency of your financial and employment information till your loan closes.

Pre-approval procedure during home search helps you find the ideal lenders, interest rates and best deal. Shop mortgage lenders within 45 days for minimum impact on your credit score.

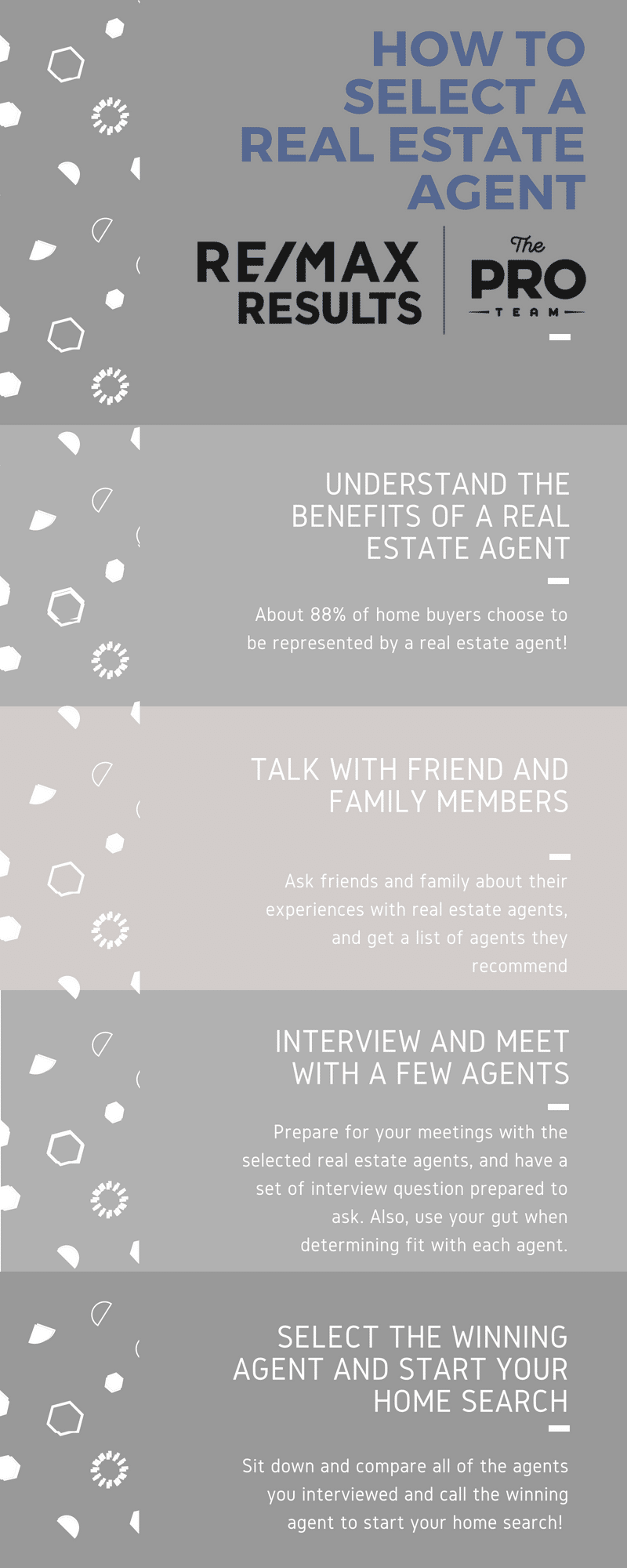

Select a Real Estate Agent

When you’re ready to buy your first home, choosing a real estate agent requires scrutiny. A knowledgeable agent becomes your navigator in the neighborhood.

Understand Your Local Market

The agent’s understanding of local schools, transportation, amenities, and housing market can provide valuable advice. Such insights can help you assess if the property aligns with your needs.

An Agent’s Network is Your Network

Ideally, your agent should have a robust professional network, including mortgage brokers and home inspectors. This network can save you from the hassle of finding these services independently. HuffPost shares worthwhile insights on this subject.

Communication is Key

Beyond their technical knowledge, an agent’s communication style matters. A proactive, personable agent helps keep you informed without overwhelming you.

Negotiation Expertise is Crucial

You will be best served by an agent skillful in negotiation. As buying a home is often emotional, having someone to effectively represent your interests will be invaluable.

Embark On House Hunting

As potential homeowners of 2024 step into this journey, the first task involves comprehensive house hunting. Several top-tier industry experts have weighed in on this phase.

Expert Advice Matters

The advice of these mavens is invaluable for hopeful buyers. Their experiences and insights are resources you can leverage as you pursue your dream home.

Avoid Common Mistakes

Listen carefully, they guide first-timers to avoid common pitfalls on the road to homeownership. Make use of their expertise to dodge similar mistakes.

Plan Your Success Strategy

They suggest key strategies should be implemented for a successful home purchase. Map out your own strategy by referencing their wise counsel.

This insightful Forbes Advisor article has more details on 2024’s housing market trends.

Submitting a Purchase Offer

Becoming a homeowner often begins with submitting a formidable purchase offer. Fortunately, numerous strategies can be employed to make your submission as compelling as possible.

Among the essential aspects of this process are include down payments, contingencies, escrow accounts, and counter offers. Expert assistance can facilitate the understanding and navigation of all these elements.

- Pick a starting price: Various factors such as budget, local market conditions, and seller’s urgency impact this decision. A trusted real estate agent’s expertise might prove invaluable at this stage.

- Set your contingencies: These provisions safeguard your interests by enabling you to withdraw or modify the offer if unexpected issues arise during inspections or appraisals.

- Decide earnest money deposit: A higher deposit may help your offer stand out in competitive markets and assure the seller of your serious intentions.

- Consider writing a house offer letter: Especially in scenarios where multiple offers pour in, an earnestly drafted house offer letter could sway the seller sentiments in your favor.

After finalizing all the details, transmit your proposal to the seller through your agent. As nerve-wracking as waiting can be after this step, understand that you have already conquered a significant milestone towards homeownership by learning how to make an offer on a house. This process was detailed well in this article.

Securing Your Mortgage

When you’re ready to purchase your first home, securing a mortgage can feel overwhelming. It’s a significant financial commitment, but comprehending the process is indeed feasible.

Prioritizing your finances requires diligence and careful foresight. However, making informed choices can provide you a sense of control and propel you towards successful homeownership.

- Analyze your affordability: One should first calculate the maximum home purchasing capability. This includes savings for down payments and monthly installments.

- Assess your credit score: A good credit score not only ups your chances of mortgage approval but also can secure you a lower interest rate.

- Select the best lender: Differing terms and interest rates across lenders necessitate thorough research. Comparing lending options will guide you towards the best choice.

Educating yourself about mortgages lessens anxieties and aids in planning realistic timelines for your new home acquisition. Taking steps towards financial preparation echoes a positive undertaking.

The complexity of the mortgage securing process is undeniable. Nonetheless, comprehending its intricacies provides an informed approach while equipping you to tackle any challenges confidently.

Sealing The Deal

In summary, first-time home buyers should conduct thorough research, understand their budget, secure a preapproval letter, consider all costs, and hire professional help. These tips will simplify the buying process, allowing you to seal the deal on your dream home with ease and confidence.