Buying a house is a significant financial decision. It involves a host of factors, one of which is deciding on the most beneficial mortgage loan. There are different types of loans available, and one that is particularly attractive to potential home buyers due to its accessibility and advantages is Federal Housing Administration (FHA) loans.

Under the purview of the United States Department of Housing and Urban Development, FHA loans have made homeownership a reality for many people who might not have been able to afford it otherwise.

Lets delve deeper into some essential components that make up FHA loans:

- Eligibility Requirements: FHA loans have relatively flexible criteria to qualify.

- FHA Processing: Overall process for applying and receiving approval for these loans.

- Variety and Features: Different types of FHA loans offer distinct benefits.

- FHA Limits: Essential knowledge on the limits set for FHA loans.

- FHA vs. Conventional Loans: Comparison between traditional mortgages and FHA loans.

- Securing Your Loan: An insight into safeguarding your FHA loan process.

The complexities around FHA loans can be intimidating, but with the right guidance, it becomes much easier.

Contents

Making the most out of FHA Loans

If you’re considering an FHA loan, it’s challenging to navigate the whole process without a practical guide. That’s why resources like Realty Digest, can be valuable.

The site offers insights on various real estate topics, including mortgage loans, home sales trend, and preparing your house for sale.

Understanding FHA loans isn’t just about knowing the process; it’s also about being well informed about fast-paced housing market trends.

The more information you have, the better equipped you will be to make the most out of your FHA loan journey.

Eligibility for FHA Loans

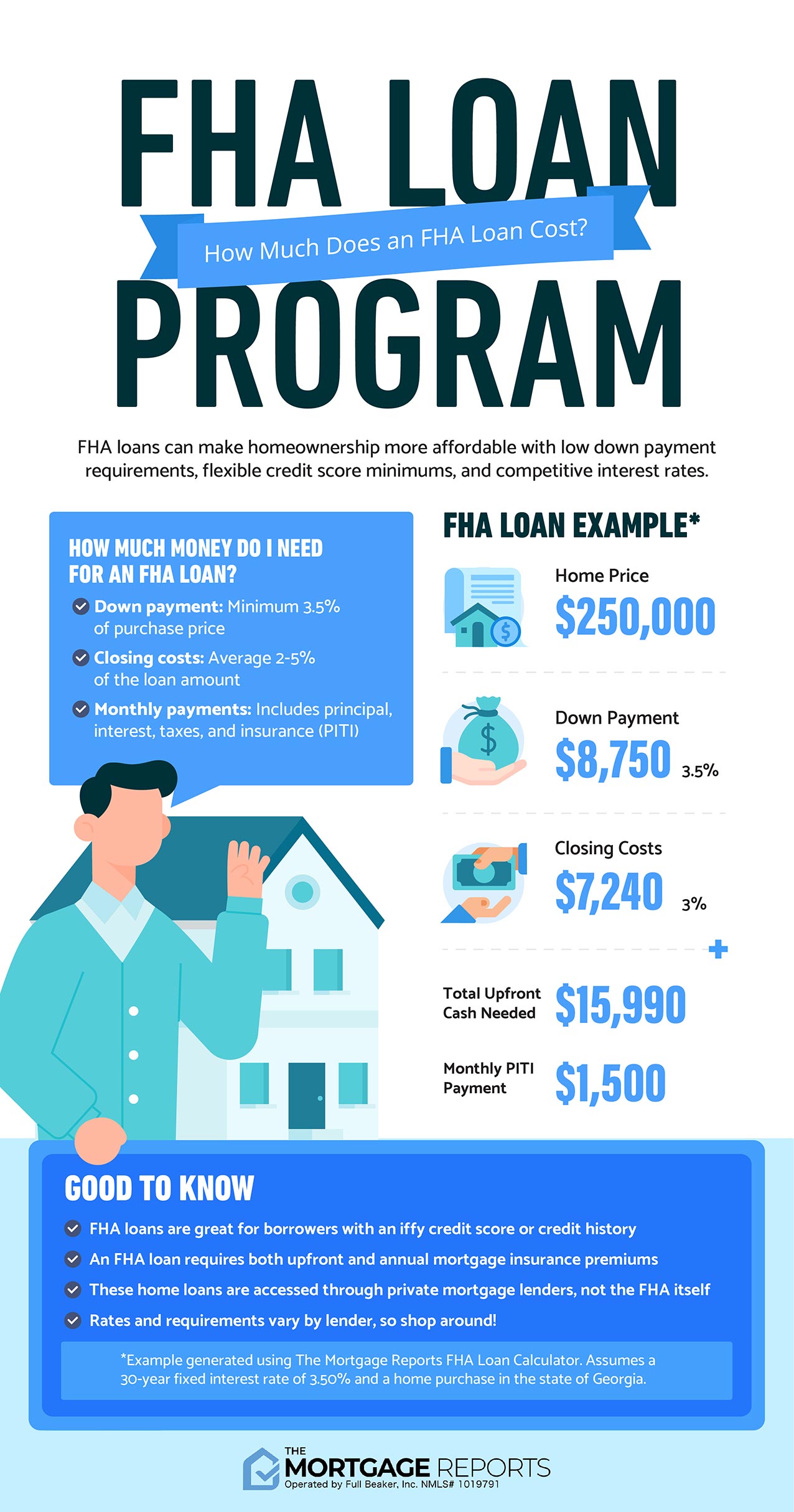

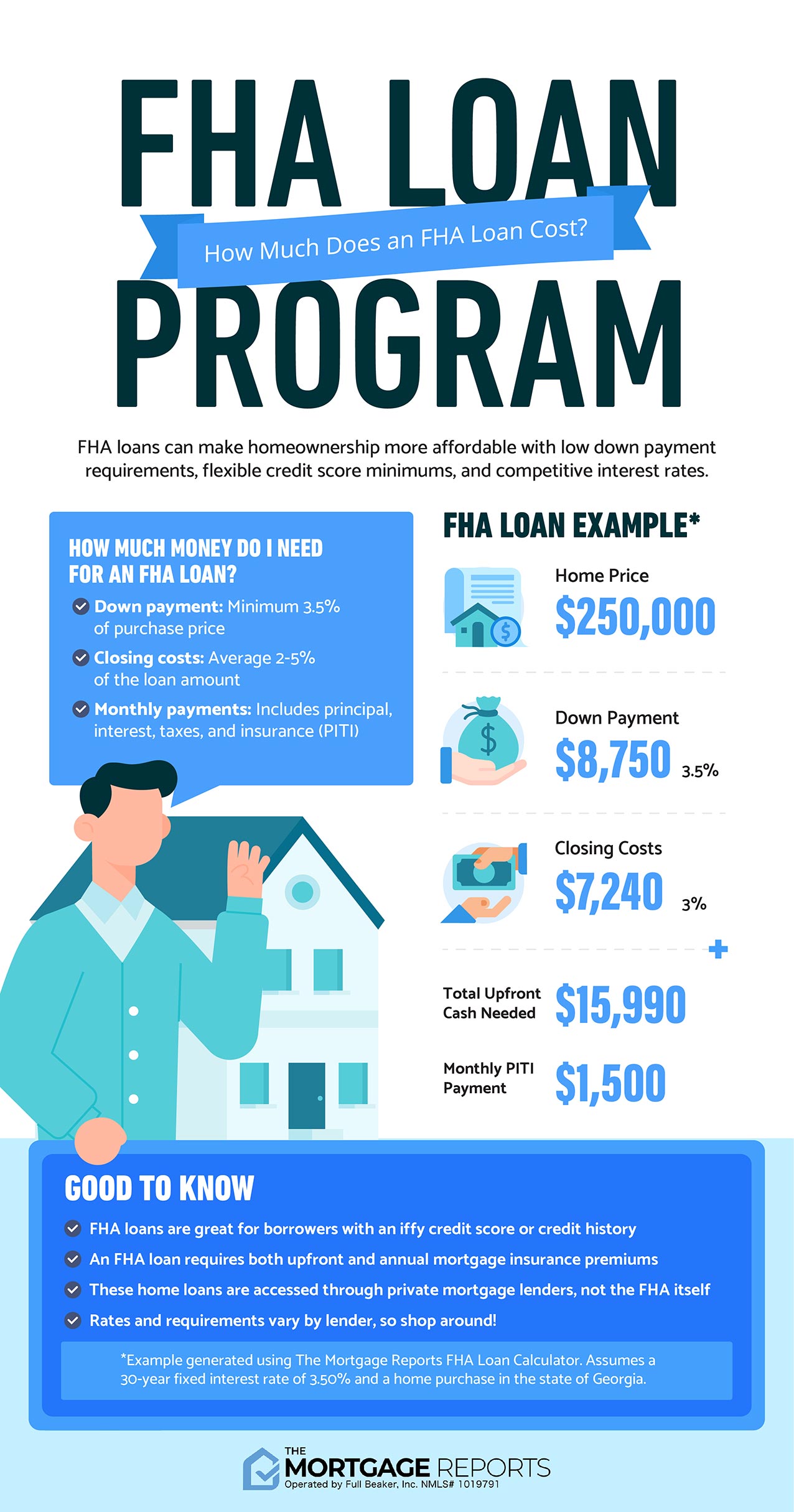

Securing an FHA Loan requires certain specifications. A standout privilege is the requirement for a minimum down payment of 3.5% on 1-4 unit properties, simplifying home ownership.

FHA loans also cater to senior citizens (62 years and older), as long as the property in question is their primary residence, and has either been paid off or has a small outstanding loan balance.

Apart from offering conventional financing solutions, the FHA loan program also provides energetic assistance via the Energy-Efficient Mortgage. This feature allows homeowners to factor in the cost of energy enhancements into their mortgage arrangement.

“FHA has financing for mobile homes and factory-built housing making it an all-rounded solution for different homeowners.”

Besides that, FHA steps in with two special products: one for those owning land upon which the house stands and another for mobile homes located or soon-to-be in mobile parks.

Lastly, programs spearheaded by state and local governments can provide significant help with your down payment requirements, find a program near you.

Processing FHA Loans

FHA loans come with the reassurance of mortgage insurance premiums (MIPs). These consist of an upfront MIP along with an annual MIP, paid on a monthly basis.

The upfront MIP is set at 1.75% of your base loan amount. For example, this equates to a charge of $6,125 on a $350,000 loan. You can opt to pay this either at closing or incorporate it into your loan.

- Your payments go into an escrow account managed by the U.S. Treasury Department. Should you default on your loan, these funds are redirected towards your mortgage repayment.

- Following the initial payment, monthly MIP payments continue. Their rates generally range from 0.15% to 0.75% annually of the loan amount, dependent on factors such as loan size, loan duration, and the property’s loan-to-value ratio.

- If your annual MIP rate is currently 0.55%, a $350,000 loan would lead to an annual MIP payment of $1,925 or $160.42 per month. This is separate from and in addition to the one-time upfront MIP payment.

- The requirement for annual MIP payments can extend up to 11 years or potentially for the complete life of the loan, largely based on the duration of your agreement and the property’s LTV ratio.

FHA loans offer unique attributes that provide financial safeguards while simultaneously offering potential homeowners a chance to secure property ownership.

FHA Loan Types and Features

One common and sought-after FHA loan is the Fixed-Rate, offering a steady interest rate throughout its lifetime, typical terms being 15 or 30 years.

The Adjustable-Rate variant provides a lower initial interest rate that may change periodically, contingent on market behavior leading to varying monthly payments.

- FHA 203(b) Loans: The go-to choice for most borrowers, furnishing nearly full financing for a property.

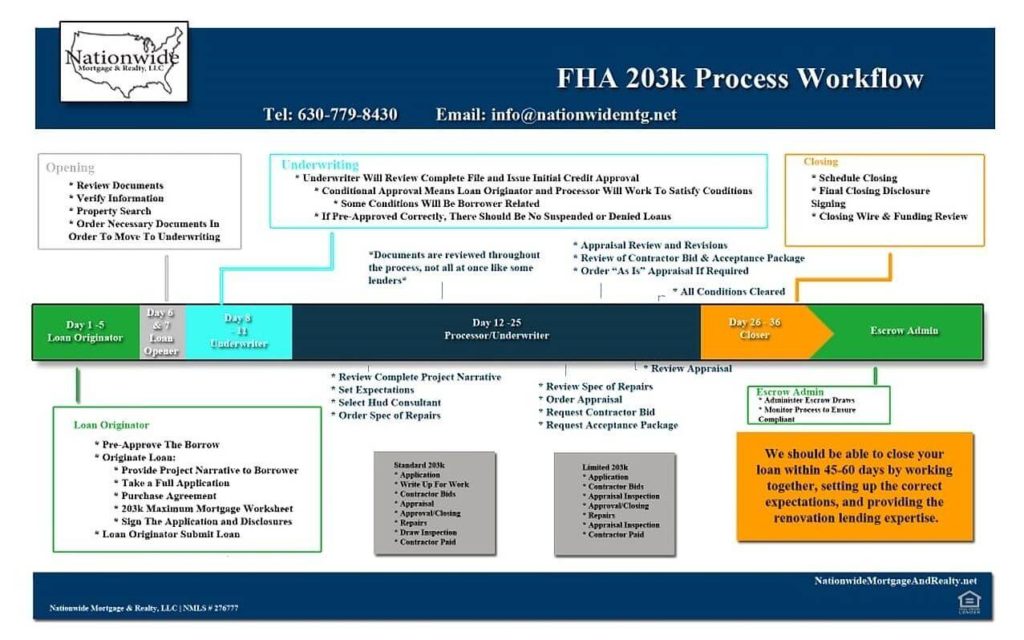

- FHA 203(k) Loans: Tailored for individuals who are property shopping and also need funds for necessary renovations.

- FHA Streamline Loans: Special refinancing options for current FHA borrowers with less paperwork involved.

- FHA Energy Efficient Mortgage (EEM) Loans: Enables financing of eco-friendly home upgrades into the main mortgage.

The FHA 203(h) Loan option supports those who have lost their homes in federally declared disaster locales finance a new residence.

The unique FHA Section 245(a) and 245(c) Loans provide mortgage plans that anticipate future income growth. These arrangements begin with small payments that progressively increase over time.

- FHA Good Neighbor Next Door Loans: Offers favorable financing to community pillars like law enforcement officers, teachers, firefighters, and EMTs.

- FHA Reverse Mortgages: An option specifically available to homeowners who have equity in their homes.

This comprehensive mix of loans addresses diverse financial conditions and needs.

Understanding FHA loans starts with knowing about their dynamic limits. The 2024 FHA Loan Limits differ depending on the unit size and location.

FHA Loan Limits in Detail

The FHA sets loan limits for one-unit homes at $498,257 in most areas. However, in high-cost areas and premium locations like Alaska or Hawaii, these limits significantly increase.

Comprehending Minimum Requirements

A minimum credit score and down payment are prerequisites for acquiring an FHA loan. Borrowers with higher scores have lower down payment obligations.

Mortgage Insurance and Debt Ratio

Borrowers should also consider the mandated mortgage insurance for the loan duration and their debt-to-income ratio, which shouldn’t breach 43%.

Loan Limit Calculation

FHA bases the loan limit calculation on national conforming loan limits. Their “floor” is 65% of this limit whilst the “ceiling stands” at 150%.

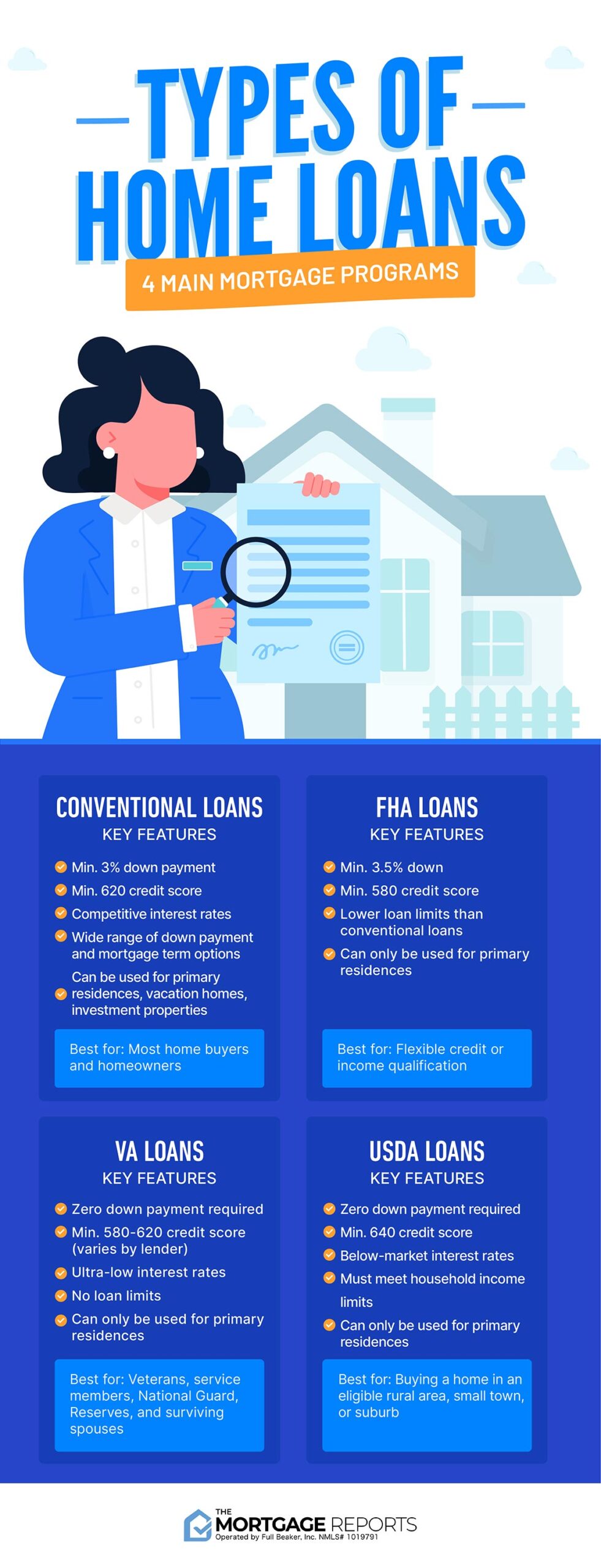

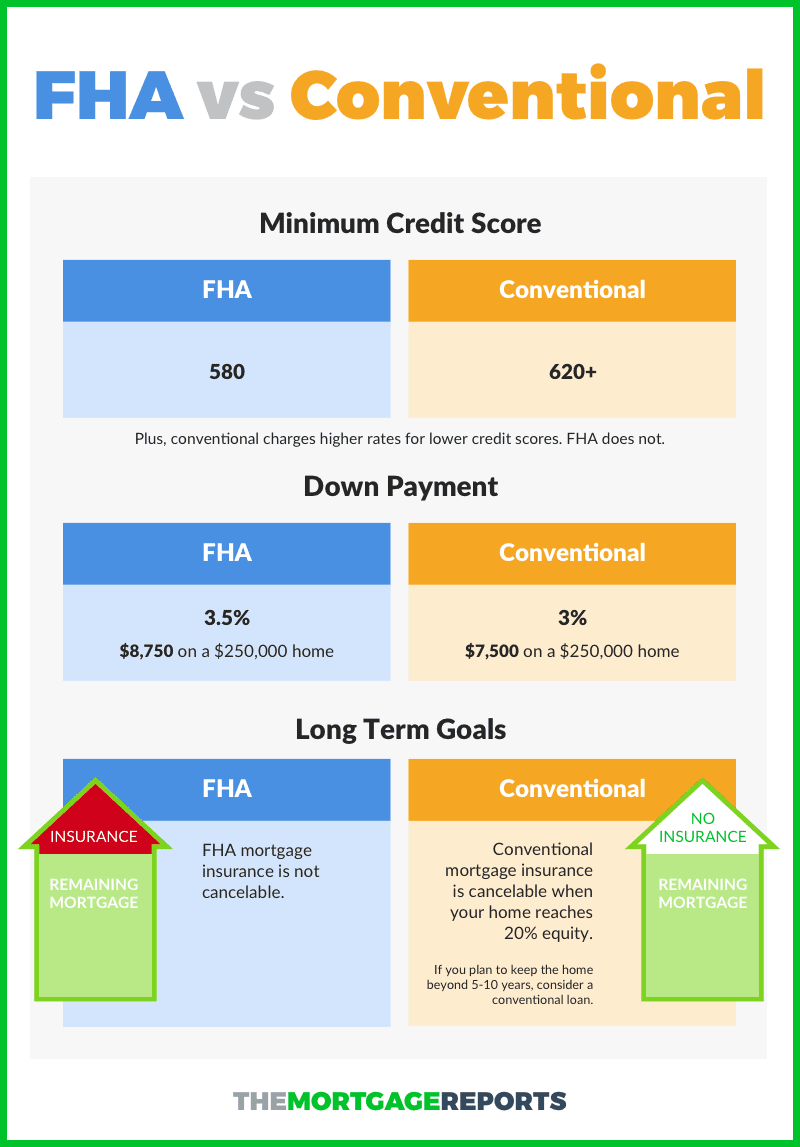

FHA Loans Vs. Conventional Loans

Considering the differences between FHA and conventional loans is essential.

Is there a loan that requires no down payment?

Yes, unlike FHA and conventional loans, VA loans don’t require a down payment.

What about mortgage insurance?

Mortgage insurance isn’t required with VA loans, contrary to both FHA and conventional loans.

Is there any fee involved?

There’s a one-time VA funding fee. The percentage ranges from 1.25 percent to 3.3 percent depending on specific circumstances.

To learn more about these specifics, you can refer to this informative article.

Securing Your FHA Loan

The FHA has been aiding first-time homebuyers since 1934. Traditional lenders such as banks issue these loans, but what makes them different is they are insured by the FHA.

This grants a lower risk to lenders, promoting better loan conditions for the borrower.

Please note these key features:

- Low Down Payments: FHA loans require only 3.5 percent down payment.

- Incorporated Closing Costs: Many of the closing costs can be incorporated in the loan itself.

- User-friendly Credit Qualifying: FHA loans have relaxed credit qualifying guidelines. Consistent bill payment history can help you qualify even without a high credit score.

- FHA Maximum Financing Calculator: Use this tool to understand how much you can borrow. It takes into account various factors like sales price of the home, appraised value, closing costs, and mortgage insurance premium.

In addition to these, FHA offers different types of loans to suit varying homeowner needs.

If your desired house requires repairs, a unique type of FHA loan allows the cost of fixes to be rolled into the primary mortgage loan.

FHA also accommodates seniors and those wanting to effect energy improvements in their homes.

It even has provisions for those who wish to purchase manufactured or mobile homes.

An essential part of what makes FHA loans attractive to newcomers is their easy qualification process based on your payment history rather than an immaculate credit rating.

Finally, be aware that the FHA sets caps on how much you can borrow based on where you live or where you plan on buying a home.

Pros And Cons of FHA Loans

FHA loans, insured by the Federal Housing Administration, attract buyers with limited savings or lower credit scores due to their feasible conditions.

Provisions of FHA Loans

These loans permit down payments as low as 3.5% for borrowers with a credit score of 580 or higher while imposing a 10% requirement for those with a 500 FICO score.

Ideal for a variety of property types, these loans facilitate the purchase of single-family houses, multi-family homes and manufactured homes with permanent foundations. Moreover, FHA loans allow refinance opportunities.

Requirements for FHA Loans

Potential borrowers need a minimum credit score of 580 alongside a 3.5% down payment. If the borrower’s credit score is 500, they require a 10% down payment.

FHA borrowers must comply with the debt-to-income prerequisite, which prefers lenders maintain a ratio less than 50%.

The Upsides and Downsides of FHA loans

FHA loans come with low down payment requirements and lenient credit score necessities. They can be used to finance multiple property types and can be utilized for both purchases and refinances.

However, if the down payment is less than 10%, mortgage insurance will be mandatory for the life of the loan. They typically have higher interest rates compared to conventional loans and stricter property standards due to required FHA appraisal.

FHA Loan FAQs

FHA loans, as government-backed mortgages, are insured by the Federal Housing Administration. They are renowned for their lower credit score and down payment requirements.

These loans are frequently sought after by first-time homebuyers. The minimum qualifying credit score for an FHA loan is 500, although most lenders ask for a credit score of 580 or higher.

Naturally, a higher credit score can afford borrowers more favorable loan terms. Additionally, the minimum down payment for FHA loans stands at 3.5% of the purchase price.

This is lower than the requirements for various conventional loans. In terms of interest rates, FHA loans typically present competitive, if not lower rates than conventional loans.

FHA loans also provide the freedom to pay off your loan at any time, including via refinancing. Furthermore, they come with adjustable-rate and fixed-rate mortgages spanning between 15 to 30 years.

Mortgage Insurance Premiums (MIPs) are always a requirement for FHA loans. MIPs consist of an upfront premium as well as ongoing monthly premiums.

Example: The period in which MIPs must be paid will vary depending on the percentage of down payment made.

The maximum loan amounts permitted under FHA loans are determined by the cost of living in your location. All properties need to satisfy specific safety standards to qualify for an FHA loan.

The application process includes pre-qualification involving self-reported financial evaluation without impacting your credit score. Pre-approval, conversely, necessitates a hard credit check and document verification.

Getting advice from local real estate agents could be advantageous when navigating this process. Interestingly, compared to conventional loans, FHA loans are generally easier for first-time buyers to access due to lenient credit score and down payment requisites.

FHA loans also impose Mortgage Insurance Premiums not prevalent in conventional loans. FHA loans can also be used for home purchasing and refinancing.

Programs such as the 203(k) permit home improvements and refinancing to be combined into one loan. Lenders might have various eligibility requirements, providing an array of choices for homebuyers.

Alternative lenders offer supplementary options, with online platforms often presenting streamlined processes and competitive terms.

FHA Loans Unraveled

FHA loans present a viable option for first-time homebuyers, offering lower down payments and lenient credit score requirements. These government-insured mortgages can significantly reduce barriers to homeownership, making them an excellent choice for those entering the real estate market for the first time. It’s essential to understand the ins and outs before diving in.