Exploring the landscape of government assistance programs can truly transform an individual’s financial circumstances. Numerous resources are available to alleviate financial strain and provide much-needed help, particularly in relation to homeownership. It is vital to understand the essentials of these programs, such as who they cater to, their varieties, and how to access them.

To simplify this complex topic, I’ve distilled key highlights into the following points:

- Mortgage Assistance Highlight: This is an overview of the resources available within government assistance programs for mortgages.

- Qualifying Candidates: These are the individuals who meet the criteria for mortgage assistance.

- Program Types: Delve into an assortment of mortgage assistance programs including loan modification, refinance options, and more.

- Access and Application: Knowing where and how to apply is crucial in benefiting from these resources.

- Addressing Financial Hardships: If you’re facing a difficult time financially, government assistance programs can provide viable solutions.

Weaving through this jargon can be overwhelming but gaining information about these schemes can make navigating considerably easier.

Contents

Understanding Government Assistance Programs

The rapidity of a house sale in today’s fast-paced real estate market is documented wonderfully here. However, government assistance programs can greatly influence your financial capability in such decisions.

Beyond the speed of transactions or the surface value of a property, it’s the underlying financial stability that governs our choices.

Every homeowner should have a clear comprehension of these assistance platforms because they offer significant support in times of need.

These programs are designed to help you weather financial storms and make beneficial decisions, especially when aiming for swift house sales.

Highlighting Mortgage Assistance Resources

If you’ve been affected by a disaster, there is hope. Federal assistance is available to help homeowners and renters alike.

FHA’s Mortgage Insurance for Disaster Victims

The FHA’s Section 203(h) program offers invaluable assistance to individuals and families who have lost their homes due to disasters.

Borrowers can access 100 percent financing, inclusive of closing costs, from participating FHA-approved lenders.

To benefit from this insurance, applications must be submitted within a year of the declared disaster.

Rehabilitation Mortgage Insurance Program

The Section 203(k) program is another lifeline available. This unique facility allows disaster survivors to finance house purchases or refinance along with the required repairs.

Also, owners of damaged houses can finance the rehabilitation of their properties using this resourceful program.

Applying for FHA Programs

To explore these programs, applications should be made through an FHA-approved lender.

The FHA Resource Center can provide further information about these valuable amenities.

Who Qualifies for Mortgage Assistance

Mortgage assistance programs are generally designed to assist homeowners facing financial hardships. For example, joblessness or underemployment due to relentless epidemic forces

If you’re experiencing an income cutback or a rise in expenses, there might be options available. The loss in income can suddenly jeopardize your home stability.

Facing Financial Struggles

Financial difficulties not only disorient your payment capacity, but also resound stressfully on every aspect of life. Certain mortgage relief programs can robustly support during such turbulent periods.

This could extend to hardships including illness, a spouse’s death, divorce or another major event. Nobody is prepared for these unforeseen life events.

Military Personnel Eligibility

Military staff may also qualify for mortgage relief if reassigned or on active duty. Upholding our heroes’ dignity is pivotal to a sensitive society.

For more in-depth information on qualifications and procedures, explore mortgage assistance eligibility. Remember: Every single family deserves a secure home.

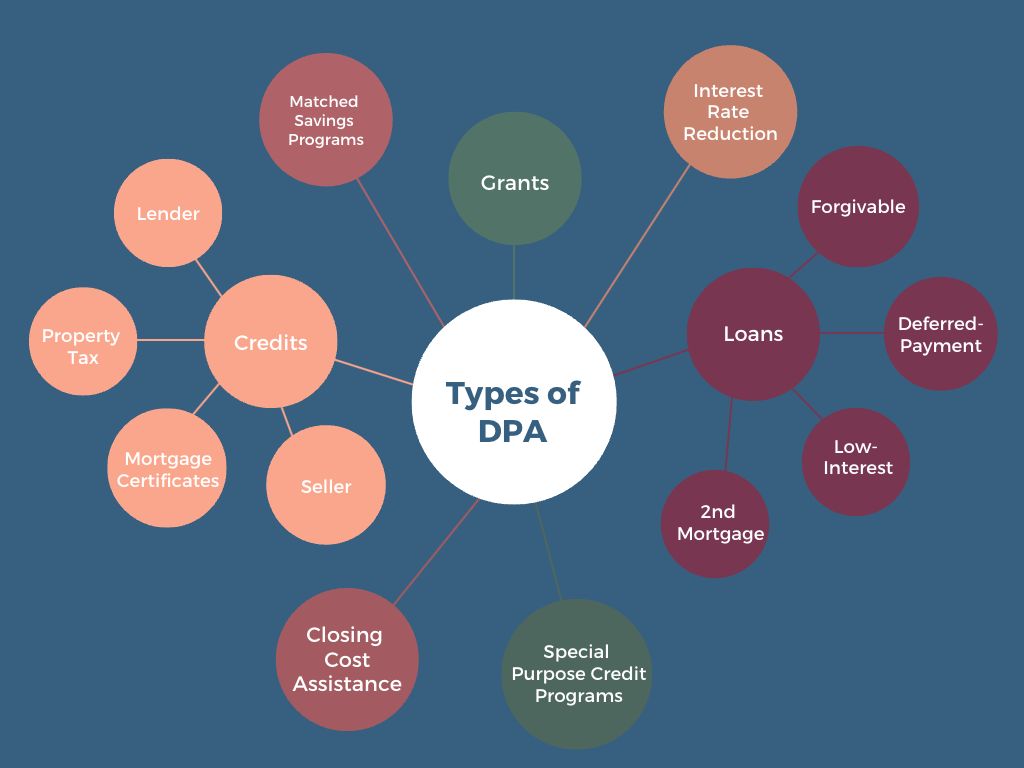

Types of Mortgage Assistance Programs

The first step towards financial stability can often be understanding the various forms of government aid available.

Mortgage assistance programs form a significant part of such aid, especially for anyone grappling with mounting debt.

Under these programs, opportunities range from loan modification to mortgage refinancing, foreclosure prevention, and more.

- Loan Modification: This option helps by altering the terms of the original loan. It’s geared towards making payments more manageable.

- Mortgage Refinancing: Refinancing entails replacing the existing loan with a new one that has better terms.

- Foreclosure Prevention: These programs provide counseling and other resources aimed at preventing foreclosure.

Anchoring on the aforementioned initiatives could significantly improve financial health and security. It’s crucial to research deeper into these programs for comprehensive knowledge.

Remember, each program comes with specific eligibility requirements and benefits, making an informed selection paramount.

Accessing and Applying for Assistance

Finding help with housing costs can be challenging. However, multiple programs exist to aid renters facing financial difficulties.

Information about these programs can be searched online. Look for rental assistance in your city, county or tribal area.

Your local government offices may be able to offer guidance. Visiting your town hall or representative’s office might uncover available resources.

Community organizations like libraries or cultural centers may also host helpful information, as well as hotline 211 which is dedicated to assisting with bill payments.

| Resource | Contact |

|---|---|

| Town Hall / Representative Office | Contact directly |

| Library / Cultural Center | Visit in-person |

| 211 Hotline | Call via landline or mobile |

| Housing Counseling Agency | 800-569-4287 |

| Above mentioned are some options for accessing help around housing costs. | |

This table serves as a basic guide to seeking financial aid for housing expenses in your area.

Note: After applying for rental assistance, expect a waiting period of several weeks before receiving funds.

If eviction is a concern, seek out related resources immediately. Consider local energy assistance programs for help with utility bills.

Housing counselors can guide you through the process and connect you to additional resources. Some agencies offer low- or no-cost rental housing counseling.

The U.S. Department of Housing and Urban Development offers programs to subsidize rents for low-income tenants.

These can include housing choice vouchers, also known as Section 8, which can be used to rent privately-owned housing and offset rental costs.

What To Do In Financial Hardships

Navigating financial hardships is undeniably daunting. However, scenarios resembling Melinda’s—a 56-year-old in Minnesota struggling to afford basics—are becoming increasingly common.

The dilemma arises when an individual earns ‘just enough’—an amount too much for aid, but below the middle-class threshold. It’s crucial to understand this peculiar socio-economic group which now constitutes about 29% of the US population.

Understanding ‘ALICEs’ or Asset-Limited, Income-Constrained, and Employed families is a step forward in demystifying financial affordability barriers.

Looking at Melinda’s monthly budget—approximately $1,500 from Supplemental Security Income benefits—it’s clear that most of her expenses go towards rent and utility bills. Her lack of full-time employment due to medical conditions—and limited income support from her husband due to his health issues—compounds these challenges.

These monetary constraints force many like Melinda to jiggle between paying for necessities and securing a roof over their heads. Negotiating flexible payment arrangements with landlords becomes necessary—though they’re often overshadowed by eviction worries.

Escalating energy costs, especially in areas with extreme temperatures like Minnesota, push the annual electricity bills to nearly $5,000—a daunting figure indeed! The importance of improved insulation becomes evident here.

Food pantries have served as valuable resources during these dire times—providing canned goods and other essential consumables. However, the options available are dwindling and do not suffice anymore.

A steady, reliable healthcare plan remains elusive for those navigating ‘ALICE’ conditions. Despite Medicare coverage and basic healthcare plans from employers, families deal with substantial out-of-pocket expenses on medications—often exceeding $350 per month.

Conclusion

Government assistance programs offer a lifeline to homeowners struggling with mortgage payments. They provide options like refinancing, loan modifications, and forbearance that can significantly ease financial burdens. It’s crucial to research and understand the specifics of these programs to make an informed decision that aligns with your financial situation.