The world of mortgages is intricate and fluctuating, with time mortgages being a prime example of its volatility. Having an intuitive grasp on how time mortgages work can greatly influence your borrowing power and financial well-being.

As we delve into the conundrums of time mortgages, let’s familiarize ourselves with the key steps integral to any mortgage planning processes.

- Preparing for Application: An essential step in securing a time mortgage is to adequately prepare your application.

- Steps for Low-Down Payment Loan: Methods to secure this type of loan can significantly empower you in a time mortgage context.

- Applying Down-Payment Assistance: Utilization of assistance programs can relieve pressure when managing time mortgages.

- Navigating Rates: The choice between fixed and adjustable rates can dramatically influence your time mortgage commitments.

- Government-backed Programs: These offerings should not be overlooked, especially when considering time mortgages.

- Choosing Lenders: Comparing various mortgage lenders is key to securing the ideal terms for your time mortgage.

In real estate transactions, timing is everything. Even a slight delay or speed-up can have immense effects on the outcome, which is particularly relevant with regard to time mortgages.

Contents

- Preparing for your Mortgage Application

- Steps to Secure a Low-Down Payment Loan

- Utilizing Down-Payment Assistance Programs

- Choosing Between Fixed and Adjustable Rates

- Exploring Government-Backed Mortgage Programs

- What are Some Commonly Used Mortgage Programs?

- What Options are There for Homebuying or Refinancing?

- How About Options for Renovating or Building a Home?

- What if I’m a Senior Looking for a Home Loan?

- Are There Special Provisions for Manufactured Homes or Lots?

- Can I Get Support for Energy-Efficient Improvements?

- What if I’m Buying on Hawaiian Home Lands, Indian Reservations, or Other Restricted Lands?

- Maximizing Employer-Sponsored Mortgage Programs

- Getting Involved in Home Buyer Workshops

- Deciding When to Lock Your Mortgage Rate

- Comparing and Choosing Mortgage Lenders

- Mastering Mortgages

A Peek into Rapid House Sales

A deeper understanding can be gained from this article on rapid house sales: How Rapid Can a House Sale Happen in 2024?. It excellently illustrates the relationship between market speed, sale timings, and their subsequent effects on time mortgages.

Whether you’re a seasoned homeowner or a first-time buyer, mastering the intricacies of time mortgages could be a game-changer in your real estate endeavors.

Remember, being well-prepared and well-informed is half the battle won!

Bearing this in mind, I encourage you to dive deeper into the world of time mortgages and utilize this knowledge for your benefit.

Preparing for your Mortgage Application

An integral element of applying for a mortgage is ensuring your credit report is accurate and up-to-date. Obtain your credit reports from the three leading bureaus and meticulously check for errors.

Improving Your Credit Score

Achieving an admirable credit score requires effort and consistency. Prioritize paying bills on time, this can positively affect your credit history. Additionally, aim to have a low credit utilization ratio.

Indulge in open financial wisdom; avoid opening new credit accounts or closing old ones just before the mortgage application. Your actions may be construed differently than intended by mortgage lenders.

Reducing Debt Load

You also need to focus on managing your debt load effectively. Aim to keep your overall debt low. This may involve a conscientious approach towards spending, with a focus on essential expenses as opposed to discretionary ones.

Saving for Your Mortgage

To ramp up your savings, consider stashing your funds in a high-yield savings account. Furthermore, look at ways you can reduce monthly expenditures such as cancelling unnecessary memberships and services or selling items you no longer need.

The range of requisite credit scores varies depending on the size of your prospective loan. Borrowers with a credit score of 740 or higher typically qualify for the best interest rates and terms.

Steps to Secure a Low-Down Payment Loan

Your journey to a low-down payment loan begins with assessing your eligibility. Considering the baseline prerequisites like steady income, satisfactory credit, and a manageable debt-to-income ratio are essential.

It’s equally vital to be realistic about your budget. Understand exactly how much you can afford. Don’t forget you’ll need to account for mortgage insurance in your calculations.

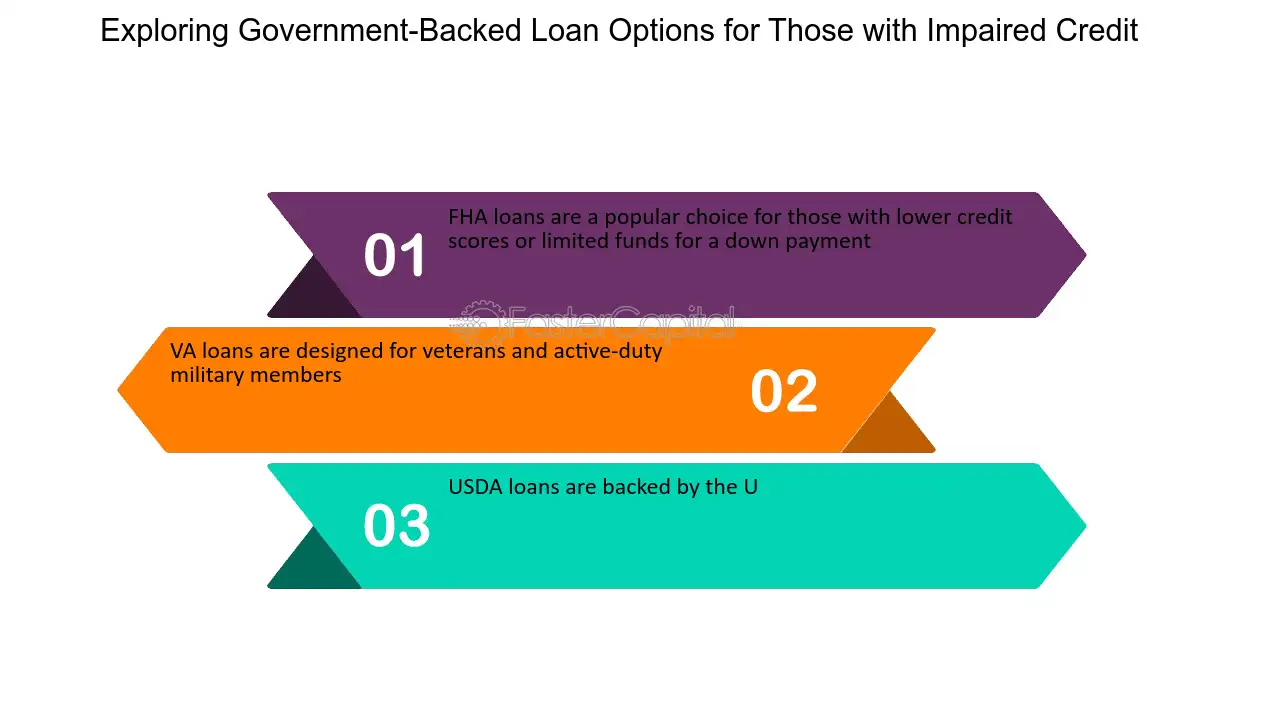

You have numerous options available to explore for down payments. The Federal Housing Administration offers loans accommodating those with decent credit scores.

On one hand, FHA Loans open doors for those who can muster a minimum 3.5% down-payment. On the other hand, Conventional 97 Loans offer the same liberty but require a slightly lower down payment of just 3%.

Several specialized programs designed specifically for low-income and first-time home buyers, such as HomeReady Loans and Home Possible Loans offer an attractive starting point.

If you meet certain criteria, USDA Loans and VA Loans offer zero down payment options. There are also tax credits available for first-time buyers through the Mortgage Credit Certificate program.

Official state and local programs can provide further support, helping with down payments and closing costs. Check out the U.S Department of Housing and Urban Development’s website for information on such programs.

In addition to these schemes, some lenders offer their own assistance programs that could potentially help you minimize down payment amounts.

Before applying, ensure you have all your financial information readily available. A meticulous preparation often results in smoother application processing. Lastly, timely follow-ups can play a key role in securing low-down payment loans.

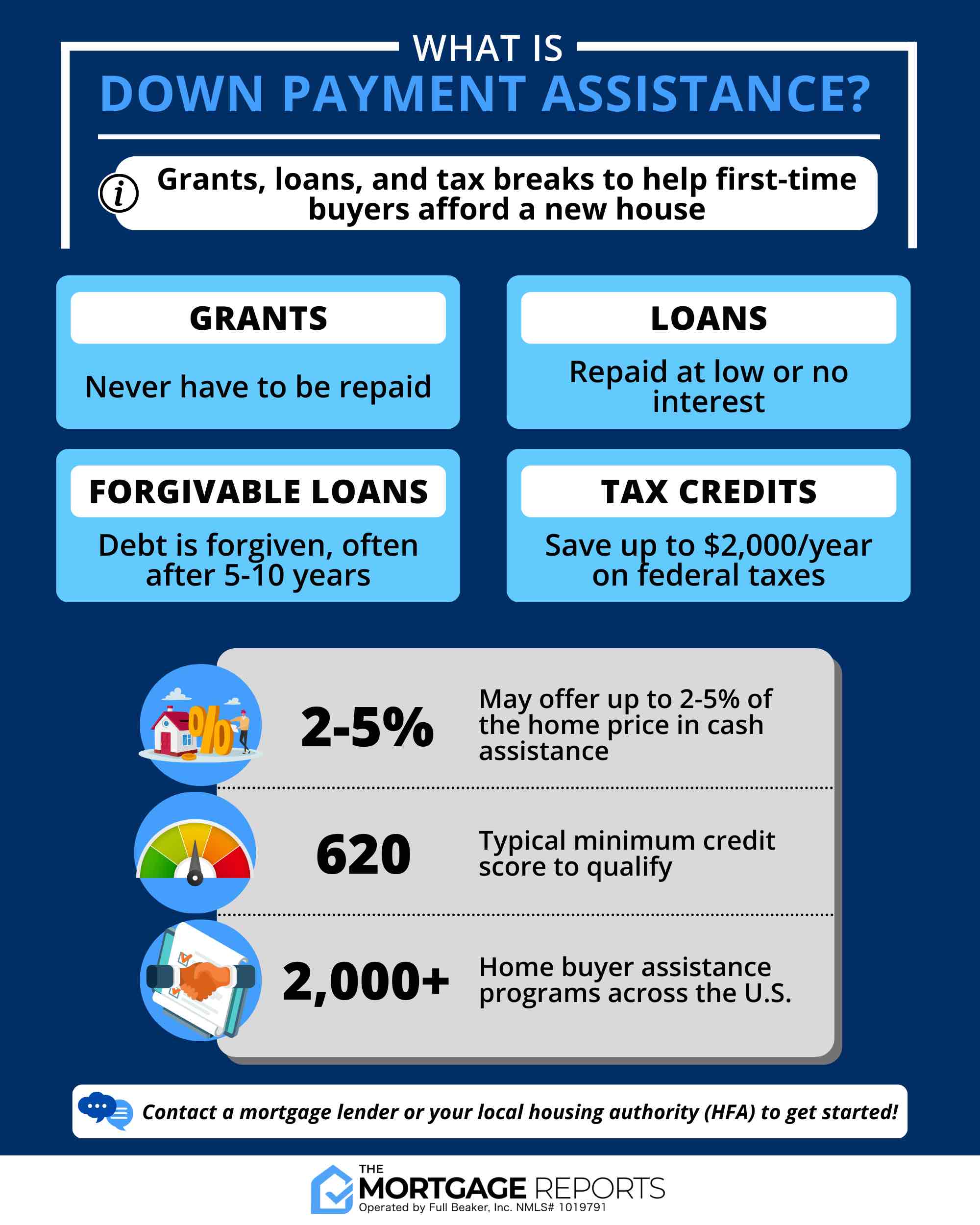

Utilizing Down-Payment Assistance Programs

Down-payment assistance programs are invaluable tools for first-time and low-income home buyers. They come in forms such as grants, forgivable loans, and deferred-payment plans.

Varieties of Financial Aid

Funds provided are designed to reduce the initial cost of homeownership. For instance, forgivable loans operate as a second mortgage with no interest.

Promisingly, they allow repayment when you decide to sell or refinance your property.

Structuring Your Aid Program

Alternatively, deferred-payment loans help cover down payments at once and allow gradual repayment over an agreed timeline at favorable rates.

Additionally, some organizations offer matching programs, increasing your down payment savings significantly.

Taking Effective Steps

To benefit from these programs, you need deliberate planning. Start by researching options available in your locality or state.

Online resources such as the US Department of Housing and Urban Development can provide comprehensive listings to guide your research.

Next, get pre-approved for your home loan to estimate your financial capacity. Real estate agents or mortgage brokers can present helpful insights on suitable programs.

Applying for Your Assistance

The application process for these schemes requires attention. Understand timing and documentation requirements to enhance your grant’s eligibility chances.

Furthermore, undergoing homeowner education courses may be mandatory with several first-time buyer programs.

After a successful pre-approval process, embark on finding a perfect fit for your financial profile. Make sure the property aligns with your program’s guidelines.

Managing Execution Timelines

Lastly, patience is crucial in leveraging these programs as the closing process may exceed the typical duration due to bureaucratic processes at play.

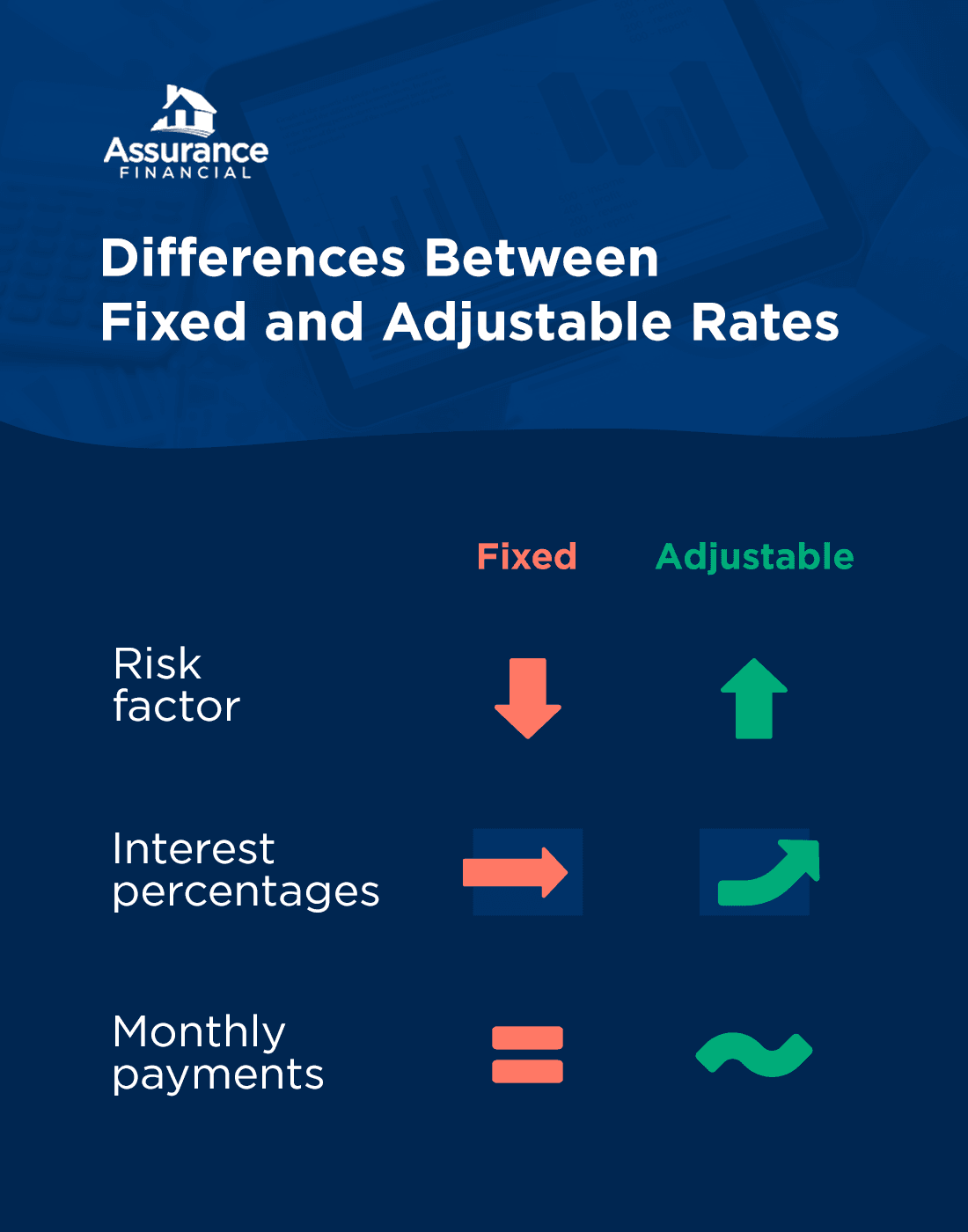

Choosing Between Fixed and Adjustable Rates

A primary distinction within mortgages lies between fixed-rate and adjustable-rate types.

Fixed-rate mortgages guarantee an unchanged interest rate during the loan’s term.

Understanding Adjustable-Rates

Unlike fixed-rates, adjustable-rate mortgages (ARMs) have variable interest rates.

The rates can fluctuate in relation with overall interest trends.

Initial Interest Rates

The preliminary rate on an ARM is often lower than a similar fixed-rate loan.

Yet, after several years, the ARM rate may exceed that of a fixed-rate loan.

Adjustment Frequency and Caps

Adjustment frequency refers to the time intervals between rate alterations.

You typically agree at loan signing to pay a rate higher than the adjustment index, otherwise known as the ‘margin’.

Also, ‘caps’ exist which limit how much your interest can change over specific periods.

Evaluating Pros and Cons

ARMs often start with lower initial payments and monthly interests. However, these amounts increase over time should rates rise.

This introduces uncertainty about future payments. Therefore, prudence remains critical when choosing between fixed and adjustable rates.

Exploring Government-Backed Mortgage Programs

What are Some Commonly Used Mortgage Programs?

Government-backed Single Family mortgage programs offer potential homebuyers and existing homeowners means to finance various housing needs.

These multifaceted plans cater to a variety of circumstances, including home purchase, construction, renovations, energy-efficiency upgrades, and more.

What Options are There for Homebuying or Refinancing?

The Basic Home Mortgage Loan 203(b), Adjustable Rate Mortgages, and Condominium Mortgages are common options.

Other avenues include Refinance Mortgages, which come in types like Streamline Refinance, Cash-out Refinance, Limited, and others.

How About Options for Renovating or Building a Home?

Mortgage plans that suit these requirements include Rehabilitation Mortgages 203(k) and Title I Home Property Improvements.

Also available are Disaster Victims Mortgages 203(h) for those affected by unfortunate events.

What if I’m a Senior Looking for a Home Loan?

If you’re over 62 years old, the Reverse Mortgage Program or the Home Equity Conversion Mortgage (HECM) might be suitable.

Are There Special Provisions for Manufactured Homes or Lots?

Absolutely. Options like Manufactured Housing (Title I) and Manufactured Home & Lot Combination exist particularly for this purpose.

Can I Get Support for Energy-Efficient Improvements?

Yes. Rehabilitation Mortgages 203(k), Title I Home Property Improvements and Disaster Victims Mortgages 203(h) can be utilized for such enhancements.

What if I’m Buying on Hawaiian Home Lands, Indian Reservations, or Other Restricted Lands?

There are provisions for these too. Options fall under Hawaiian Home Lands and Indian Reservations and Other Restricted Lands 248.

For more details, it’s suggested to visit the FHA Resource Center.

Maximizing Employer-Sponsored Mortgage Programs

Benefiting from employer-assisted mortgage programs can ease homeownership. Numerous forms of assistance are available.

The employer’s support might come as a grant, an outright repaying or forgivable second mortgage, or an unsecured loan.

Funds provided by the employer can be used to finance all or a fraction of the down payment or closing costs.

However, they must adhere to specific minimum borrower contribution stipulations. Unsecured loans are solely for use in down payments and closing costs.

| Type of Assistance | Can it be used for Down Payment? | Can it be used for Closing costs? |

|---|---|---|

| Grant | Yes | Yes |

| Fully repayable Second Mortgage | Yes | Yes |

| Forgivable Second Mortgage | Yes | Yes |

| Deferred-payment Second Mortgage | Yes | Yes |

| Unsecured Loan | Yes | Yes |

| Suitability of Assistance Programs for Use in Homeownership Finance. | ||

The funding has to originate straight from the employer, even if disbursed via a credit union associated with the employer.

If employer assistance arises as a secured second mortgage, it could be structured as a Community Seconds transaction.

Fannie Mae’s guidelines for mortgages that involve subordinate financing must be fulfilled.

If the secured second mortgage or loan doesn’t necessitate routine payments, income-to-debt calculation becomes unnecessary for the lender.

Unless, of course, periodic payments have to be made for the second mortgage at which they must be factored into the ratio.

Loan-to-Value Ratio implications also vary. For instances of 80% or less One- to Four-unit primary residences, all funds can come from employer assistance.

With LTV ratios greater than 80%, different rules apply for single-unit and multi-unit homes. Refer to HomeReady Mortgage Underwriting Methods and Requirements for further information.

Last but not least, proper documentation is key! Any assistance program must be a legitimized company scheme and not a scheme crafted for a specific employee.

The specifics of the employer’s assistance, including the terms of any other employee help provided, need to be documented comprehensively.

Getting Involved in Home Buyer Workshops

If you’re a first-time home buyer, you may be unaware of the various benefits you might be eligible for. One such perk includes tax credits, also known as mortgage credit certificates.

To qualify for these benefits, consider investing some time in a homebuyer education course or workshop. This will increase your understanding of the real estate market, helping you to make informed decisions.

- Home Buyer Courses: These classes provide vital information about the home buying process.

- Workshops: These are interactive sessions where you can ask questions and gain real-time insights.

- Tax Credits: These can significantly lessen your financial load by reducing the tax you owe.

- Down Payment Assistance: Some programs offer this to help you cover the upfront cost of purchasing your new home.

The knowledge gained from these workshops is not just theoretical. It equips you with practical insights on dealing with real-world situations. More importantly, completing these courses may open up opportunities for down payment assistance or loan forgiveness – making owning your dream home a reality much quicker than expected.

You can find more details on first-time home buyer programs and their benefits here.

Deciding When to Lock Your Mortgage Rate

Locking your mortgage rate can be a strategic move once you’ve signed a contract on a property. This prevents any rise in interest rates that might occur while finalizing the home purchase process.

Your rate can be locked for a specified period, ensuring that your housing costs stay relatively predictable. This aids with budget management and future-oriented financial planning.

- Understand the Market Conditions: Securing your mortgage rate is often dictated by economic variables that could influence mortgage rates.

- Know Your Financial Capabilities: This would help you determine whether you’re better off locking in a rate now or whether there’s room to wait and watch the market trends.

- Evaluate the Length of Rate Lock: The time frame for rate lock needs to be considered carefully based on when you expect to close the deal.

Finding just the right timing for

is paramount as it directly impacts your monthly payments and hence, the overall cost of your home.

Suffice to say, prudent decisions based on real-time data and personal financial circumstances will facilitate an informed commitment.

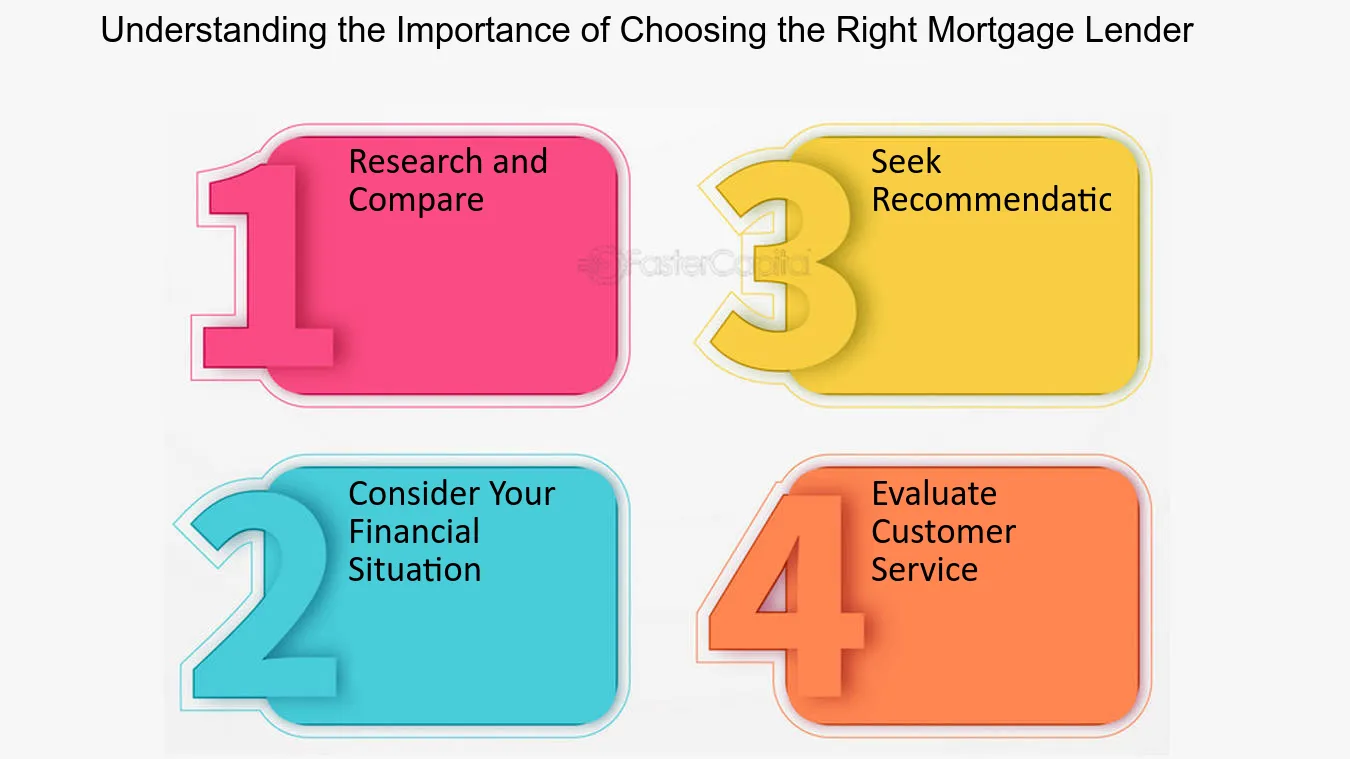

Comparing and Choosing Mortgage Lenders

Identifying your preferred loan terms is paramount. Know your financial limits and weigh them against your long-term goals.

Look for referrals. Friends and family who have gone through this process can be invaluable resources and may recommend trustworthy lenders.

- Engage multiple lenders: Don’t settle on the first lender you talk to. Engage multiple lenders to get a wider perspective.

- Examine rates and fees: Both rates and fees vary from lender to lender. Comparing these costs can lead to significant savings.

- Focus on reputation: A lender’s reputation matters. Look into their client satisfaction levels, responsiveness, and reliability.

Consistency in communication with potential lenders is key. Stay organized to effectively compare their pros and cons.

Last but not least, make a choice based on comprehensive analysis of the data gathered.

Mastering Mortgages

Securing a first-time mortgage can be daunting. However, being informed about your options, knowing the market, and planning your finances carefully can make a huge difference. The journey may seem taxing, but with patience and the right advice, you’ll be securing your dream home soon enough.