As we delve into the understanding of the Federal Housing Administration (FHA), it’s crucial to comprehend its key mechanisms and impacts. Unlike traditional financing methods, FHA prioritizes accessible homeownership, low down payments, and flexible eligibility criteria, providing stability in the housing market.

Let us break down some important aspects of the Federal Housing Administration to better understand its role. Here’s a quick list:

- Overview of FHA Programs – These are initiatives designed to facilitate homeownership

- Definition and Impact of Redlining – A discriminatory practice that has shaped many neighborhoods.

- FHFA and Climate Risk Measures – Steps taken by Federal Housing Finance Agency to ensure climate resilience.

- Exploring FHA Debentures – These are bonds issued by the FHA, a method of raising loan capital.

- Public Engagement in FHA Programs – The importance of public participation in implementing these programs.

Understanding these points paints a broad picture of how the FHA functions and influences housing markets.

Contents

An In-depth Look at The Federal Housing Administration Measures

One interesting aspect of dealing with these policies is exploring swift home sale possibilities. Recently I read an article that enlightens us on how rapidly a house sale can happen in 2024. Such information plays into crafting effective housing strategies.

Familiarizing oneself with such nuances enables better decision-making, particularly true for first-time homeowners who take advantage of FHA’s low down payment schemes.

The existence of the Federal Housing Administration has undoubtedly shaped the housing landscape, and understanding its different mechanisms allows us to appreciate its critical importance.

A more thorough comprehension of the FHA can inform more effective home-buying decisions and ensure our choices align with our long-term housing goals.

Overview of FHA Programs

The Federal Housing Administration (FHA) is a key component of the U.S. Department of Housing and Urban Development. Its primary role is offering mortgage insurance on loans granted by approved lenders.

We cater to a diverse range of property types including single-family homes, multifamily properties, residential care facilities, and hospitals. Our reach extends across the United States and its territories.

Mortgage insurance provided by us safeguards lenders from financial losses. In a scenario wherein a property owner fails to meet their mortgage obligations, we settle the claim, ensuring lenders are not left in the lurch.

- Reduced lender risk: With our insurance coverage, lenders gain confidence and increase their mortgage offerings to prospective homebuyers.

- Strict qualification criteria: We maintain certain requirements for loan qualification. Only those loans that meet these prerequisites qualify for our insurance.

Our operations are primarily sustained through our self-generated income which mainly comes from the mortgage insurance premiums that borrowers provide via lenders. These funds are utilized for managing our beneficial programs.

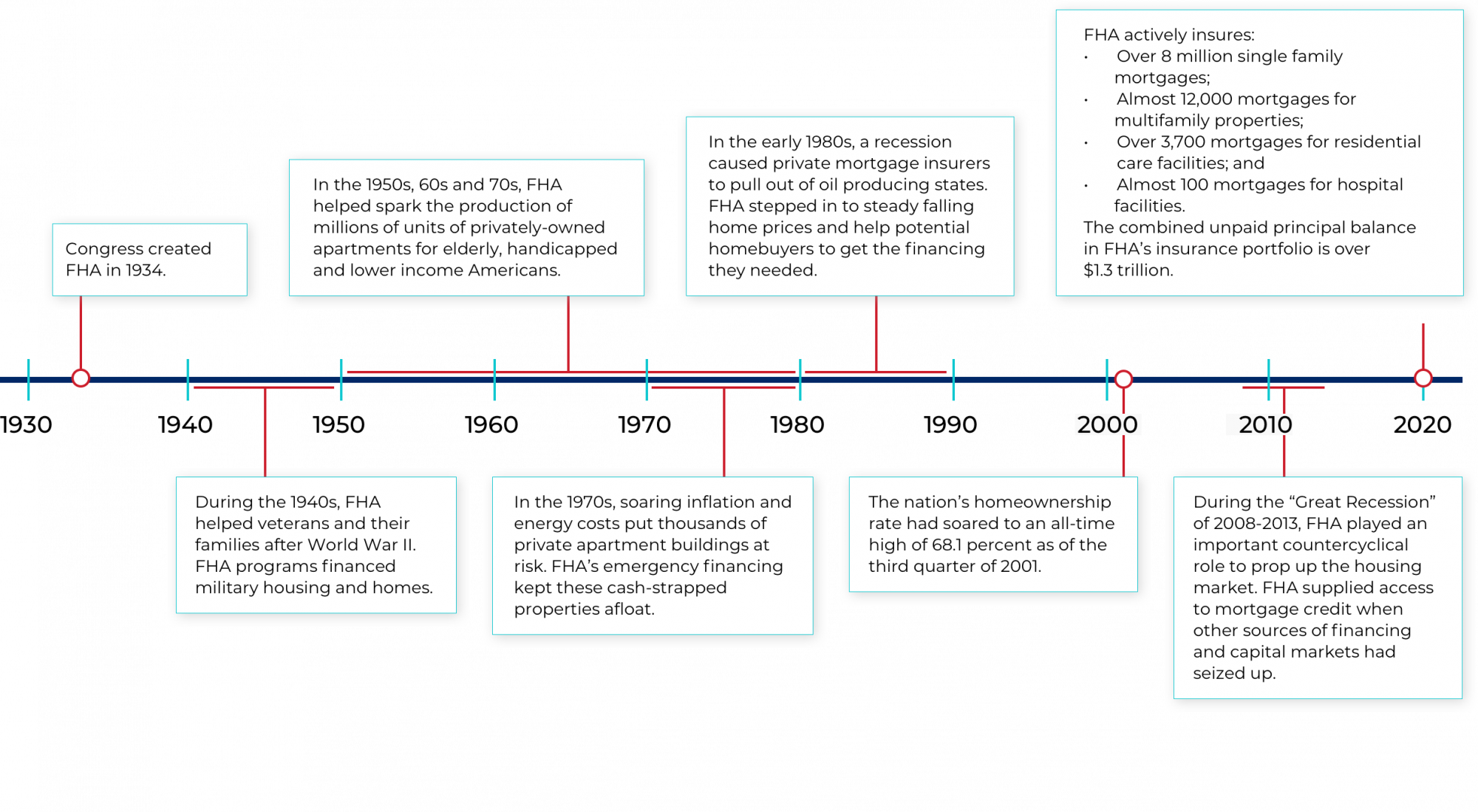

The FHA was birthed by Congress in 1934, during a period known as the Great Depression when the housing industry was in dire straits. This initiative came at a time when owning a home was only a dream for 9 out of 10 households in America.

In 1965, FHA became incorporated into the Department of Housing and Urban Development’s Office of Housing. Since then, it has continued to grow in prominence and has become an instrumental vehicle for ensuring affordable housing for all.

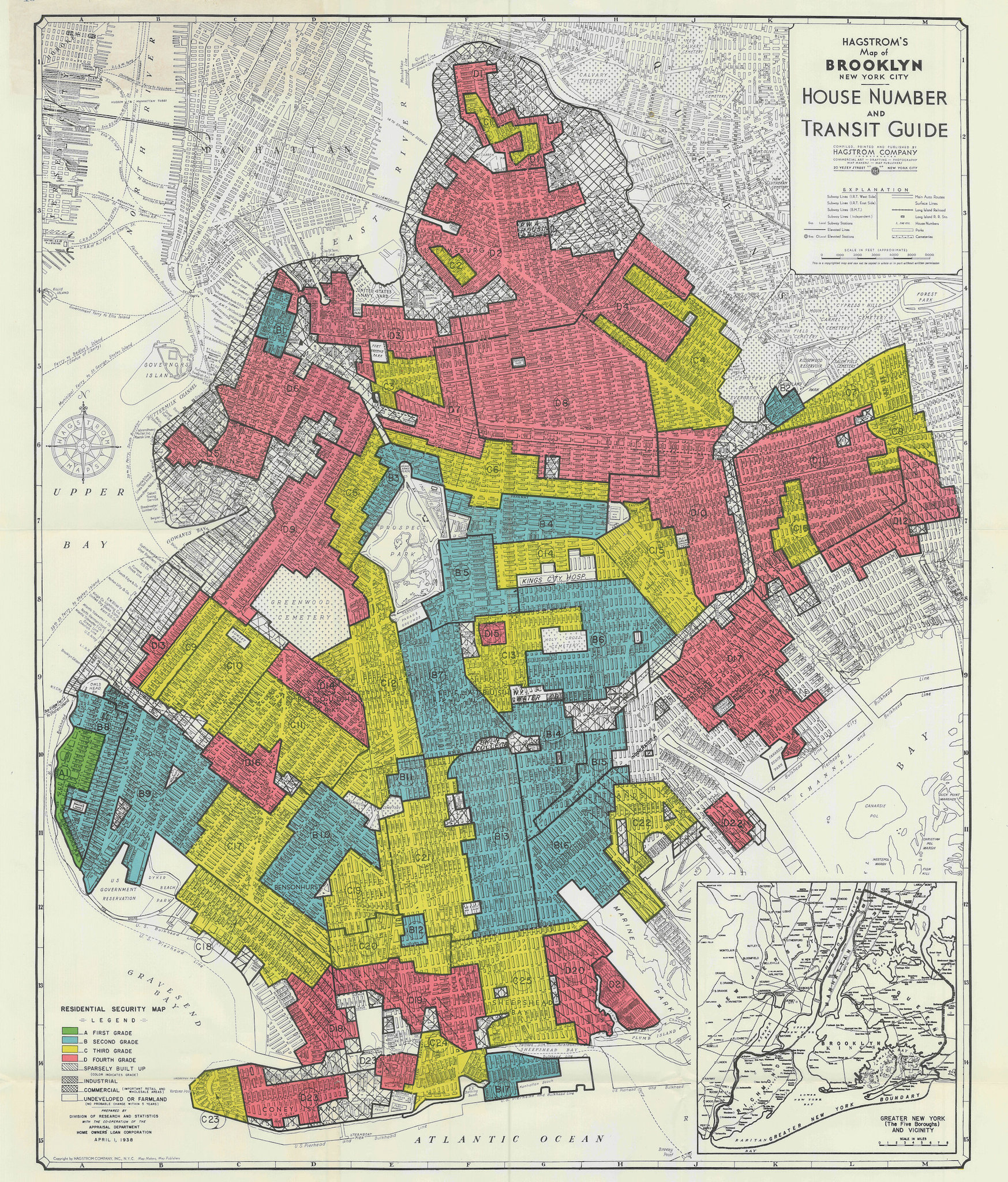

Definition and Impact of Redlining

Redlining, originating in the 1930s, used color-coding on maps to highlight “risky” areas for housing investments and mortgage loans.

This insidious practice was rooted in explicit racial assumptions, leading to legal obstruction of specific races and ethnicities from housing opportunities.

Until the Fair Housing Act of 1968 came into effect, redlining effectively barred many Black households and households of color from homeownership opportunities.

Apart from redlining, other racially biased policies included racial covenants, home loans under the GI Bill, private lending practices, urban renewal projects, and zoning laws.

The Federal Housing Administration played its part in the propagation of these policies with their own set of graded maps. These maps, however, were discarded by the agency in 1969.

While it’s true that redlining had a significant impact on discriminatory housing practices for many decades, it’s consequences persist into current segregation patterns and inequality levels.

Interestingly, past instances of redlining don’t always translate to current housing instability. Some places experience positive correlations, but others show no correlation or even a negative one.

It’s clear that issues such as air quality, temperature differences, and tree cover in redlined areas continue to be prominent concerns within this context.

Even though redlining was a major contributor to housing instability issues and subsequent market consequences affecting Black communities especially, more contemporary forms of discrimination compound the problem.

Housing instability remains more common among people of color. They’re less likely to be homeowners and more likely to carry an expensive housing cost burden as well as face forced evictions.

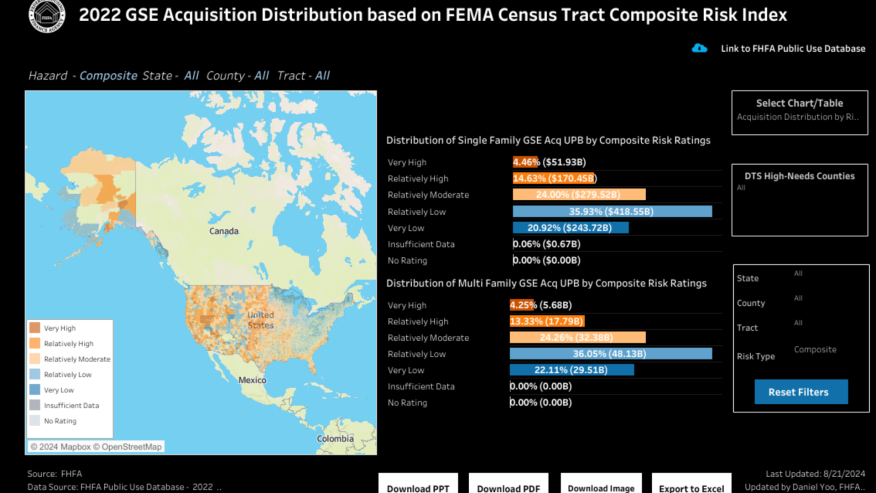

FHFA and Climate Risk Measures

The Federal Housing Finance Agency (FHFA) has implemented a Climate Risk Committee to analyze the effect of climate change on housing markets. This includes its impact on disadvantaged communities.

This committee is comprised of members from across the Agency’s divisions, with working groups focusing on different sectors such as data research and climate exposure assessment.

Furthermore, the committee also handles reporting, disclosure, governance issues, and green bonds. This multi-faceted approach ensures a comprehensive understanding of the climate-related financial risks impacting the housing industry.

The Importance of Collaboration

Cooperation has played a key role in the committee’s functions. The FHFA joined forces with several organizations to better understand and mitigate climate-related risks. These partnerships indicate the FHFA’s active involvement in addressing these critical issues.

Sharing knowledge and data is crucial in assessing climate impacts. Hence, this collaboration aims to facilitate information sharing on climate-related financial risk data. This shared knowledge enhances efficiency and helps make informed decisions.

Ongoing Work

The work by the Climate Risk Committee is crucial in ensuring stability in the housing market amidst environmental changes. More details about their efforts can be found on FHFA’s official page.

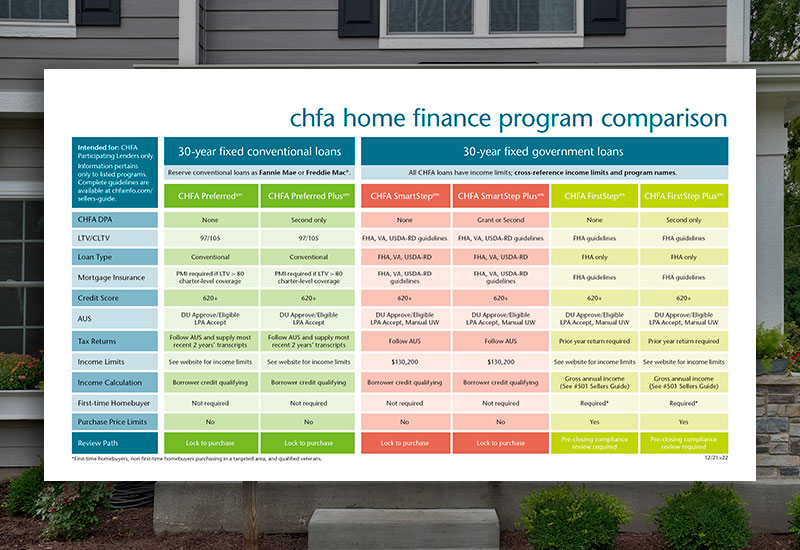

Exploring FHA Debentures

FHA loans, insured by the federal government, were created for borrowers who might find securing other loans challenging.

These loans are issued by private lenders and require two types of mortgage insurance premiums (MIPs) – one upfront and another monthly.

| Key FHA Loan Features |

|---|

| FHA loans act as an affordable option for first-time homebuyers. |

| Lower credit scores and down payments are acceptable for FHA loans. |

| The FHA is part of the U.S. Department of Housing and Urban Development since 1965. |

| Mortgage insurance must be purchased by borrowers with FHA loans. |

| The insurance premiums finance FHA’s operations. |

The insurance acts as protection against mortgage defaults.

If a borrower defaults, the FHA compensates the lender. Those with credit scores as low as 500 can still secure an FHA loan but with a minimum 10% down payment.

For credit scores of at least 580, up to 96.5% of a home’s value can be borrowed with an FHA loan. The down payment can come from various sources such as savings or gifts from family members.

It’s crucial to note though that while it insures them, the FHA does not issue loans directly. These are granted by authorized banks or financial institutions instead.

Mortgage insurance purchase is mandatory for qualifying borrowers, with the premium payments channeled to the FHA. For further insights on this topic, you may refer to this resource.

Public Engagement in FHA Programs

Federal Housing Administration (FHA), is a significant organization promoting homeownership by guaranteeing mortgages. However, problems come to play when unscrupulous lenders use deceptive tactics.

Risky lenders tend to circumvent the system, leading to potential losses for the government, hence the need for closer scrutiny on transactions. The question lies on how this can be fully ensured.

- Non-profit movements are closely studied for potential foul play to avoid the government sponsoring high-risk loans inadvertently.

- Adherence to federal regulations is required of every non-profit organization, especially with regards to their funding sources.

- The FHA’s oversight plays a critical role in ensuring that organizations remain compliant and don’t disguise risky behavior.

An anti-foreclosure ‘payment protection program’ scheme comes under intense discussion for its effectiveness. Critics suggest this approach often only postpones defaults, rather than preventing them entirely.

A well-known lender had previously faced legal action for fraudulently securing FHA guarantees on their loans, which resulted in substantial losses. Such instances lead to tighter regulation and intense scrutiny of organizations involved in FHA programs.

The FHA remains committed to stringent policing of its lending community and is ready to take immediate action upon identifying attempts at fraudulent activities. Transparency and complying with FHA requirements are emphasized to all lenders participating in these programs.

The federal tax rules specify that a non-profit cannot operate solely for private interests’ benefit. Funds generated through engagement fees and such must be utilized responsibly and within the organization’s established purpose.

FHA is keenly aware of luring marketing techniques, often meant to reduce delinquency rates and maintain lenders’ compliance with FHA requirements, and is actively working at counteracting such tactics.

The FHA Verdict

Federal Housing Administration (FHA) programs offer a lifeline to potential homeowners struggling with traditional mortgages. By providing insurance to lenders, they lower the risk of default, enabling more accessible loans. Despite potential drawbacks, like upfront mortgage insurance premiums, FHA programs democratize home ownership, especially for first-time buyers and those with lower credit scores.